Tax-Free Wealth by Tom Wheelwright Summary

CPA Tom Wheelwright explains how to minimize your taxes.

Key Takeaways

- Real estate investing gives you a tax deduction that can be used on your salary or business income taxes. This can make real estate more attractive than stocks.

- Integrate tax planning into your wealth strategy.

- Invest (in real estate) where you travel. Invest in your favorite travel destination. You can turn the travel expenses into deductible expenses.

- Almost any expense can be deductible. Any travel can be deductible by making it a business or investment expense. As long as the travel has its primary purpose as business, then all of the travel expenses, including hotel, airfare and meals, will be deductible.

- You need to find a good tax advisor. Some of them don’t know enough to help you and others are more interested in protecting their liability than helping you.

- Set up an LLC. It gives you liability protection and tax advantages of the S corp, C corp, or partnership.

- In the early years of your business, you may want to set up a sole proprietorship so you don’t have to file another tax return. (You can switch to an S corp later when you have employees.)

- Business isn’t always about doing something other people can’t do for themselves; it’s doing something they haven’t thought to do for themselves.

- You can file amended tax returns anytime, which correct errors on returns for up to the previous 3 years if you learn that you paid too much in a prior year. Or you can carry back a loss from the current year to a prior year, use the loss to offset the prior year’s income, and get a refund now.

- Every dollar you earn can increase your taxes.

- Every dollar you spend can decrease your taxes.

- The 2 keys to taxes: (1) there are certain types of income that are taxed higher than others—get low-tax income. (2) learn how to turn your expenses into tax deductions. Every expense has the potential to reduce your taxes.

- Have business meals. Discuss business and turn your meal expense into a deductible expense.

- You need to get a business credit card and use it for all of your business expenses. It gives you a list of deductible expenses. And it can give you credit card rewards points.

- Gas can be a business expense if you use your car mostly for business. If you’re self-employed or own a business.

- 3 requirements of business expenses: (1) The expense must have a business purpose, which means the primary reason for spending money was for your business. A business meal, for example, would require you to talk about business before, during, or after the meal. (2) The expense must be ordinary—not too extravagant or frequent. (3) The expense must be necessary, which means that the purpose of the expense is to make more money for your business.

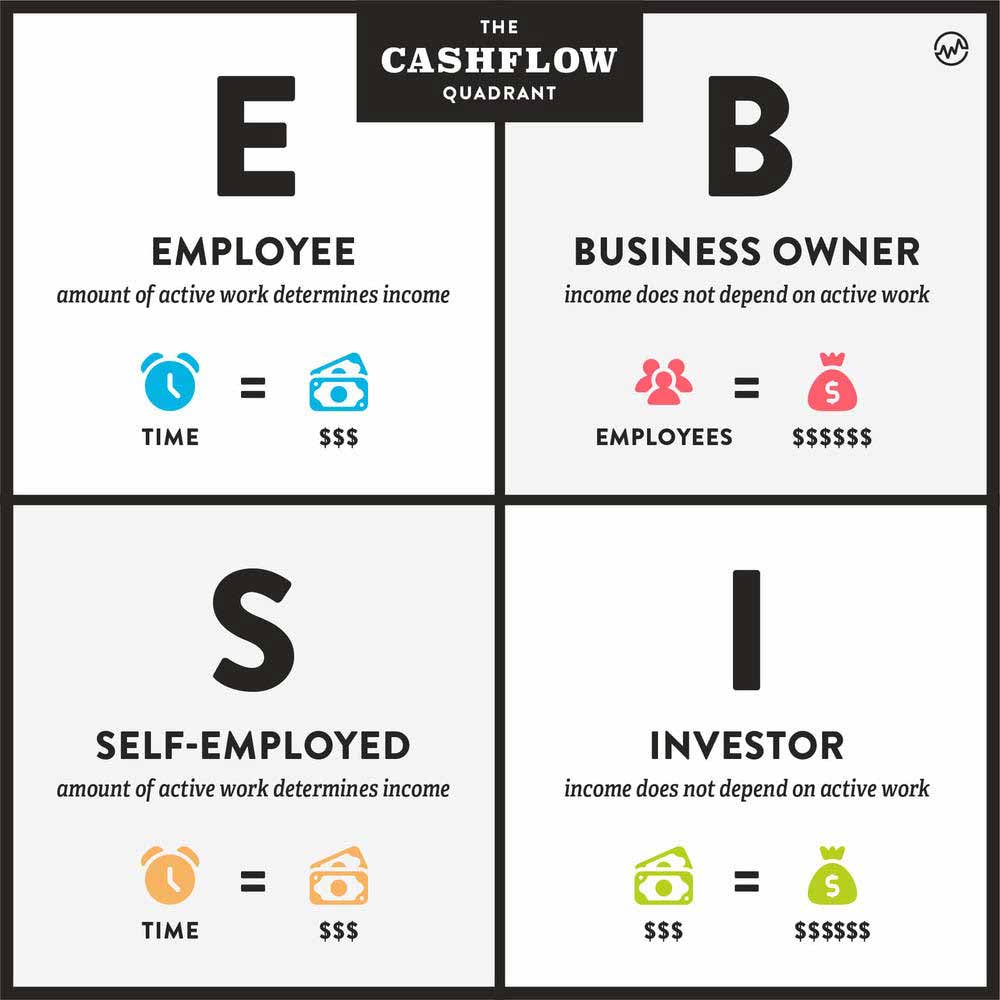

- Robert Kiyosaki was a high-end tax client of the author of this book. That’s how they met.

- Look up Robert Kiyosaki’s cashflow quadrant. Employees and self-employed individuals pay much higher taxes than big businesses and investors. Why? Because that’s what the government wanted. They want to encourage people to make businesses and invest (in real estate).

- The government gives tax breaks for oil and gas investing, farming and other agriculture, green energy, and low-income housing.

- You can deduct any travel if you spend more than 4 hours per day looking for real estate deals.

- Put your family to work. Make your business a family business. Then when you travel for business, your family’s travel is deductible. And you can shift income from your higher tax bracket to their lower tax bracket. Children are taxpayers too.

- Governments steer economic behavior through the tax code. They reward desired behavior with tax breaks. That’s why reducing your taxes is actually patriotic.

- The average taxpayer has a job, a family, and a mortgage or rent. They have little to no financial education. These people get little to no tax benefits. Don’t be an average taxpayer.

- Business expenses are the best kind of deductions. Real estate expenses are the next best.

- Your first step to increasing your deductible expenses is to become an entrepreneur or investor. But it is essential that you get a financial education first (not at college, just read books and watch educational videos). It is extremely risky to start a business without getting a financial education first.

- Start a part-time online business using skills that you already have. You can keep your job.

- What many self-employed people and small business owners don’t realize is that you can still write off your business expenses without registering as an LLC.

- A “sole proprietor” is just a fancy term for someone who works for themself and who hasn’t registered their business as its own legal entity. That’s right — as a sole proprietor you are not required to register with federal or state governments. You’re off the grid. At least until April 15, when you have to file your taxes.

- Expenses: Business use of your home office: If you regularly work at an at-home workstation, you can deduct home-related expenses like your rent and utilities — not to mention all your office furniture.

- Expenses: Continuing education: This includes any costs incurred to hone your skills or further your expertise.

- Expenses: Marketing and advertising costs: Website fees, logo designs, professional headshots — all of these count . However you decide to promote yourself or your business, it’s tax-deductible.

- Accredited investors are what the author calls “passive investors” in America.

- One of the best business or investment decisions you can make is to keep good documentation of your income and expenses. Have a file of business expense receipts on your computer. This will make any potential audit go smoothly.

- Depreciation is magic. When you buy an asset that produces income, you can deduct a portion of it each year you own it. If it’s a physical asset, such as real estate or equipment, the deduction is called depreciation. If it’s an intangible asset, the deduction is called amortization.

- Depreciation: you get to take a deduction for a portion of the building every year for a set number of years. Even though the building may not wear out for hundreds of years and may actually increase in value. That’s why depreciation is magic.

- You can depreciate the things on your property like landscaping, fencing, parking lot, floor coverings, window coverings, and cabinetry at a faster rate of depreciation—so you get to deduct money faster.

- The key to depreciation: properly document the values of all the items you depreciate on a cost segregation or chattel appraisal—even better, have a tax professional or engineer document them for you.

- You can depreciate your car if you use it mostly for business.

- If you find a $1 million apartment complex or multi-unit house, depreciation is about 3.6% per year. If you put down 3%, you only pay $30,000. And you can depreciate roughly $40,000 per year. The depreciation is used against your tax consequences and the excess is given to you in a tax refund. This gives you income every year and rental income and the property can increase in value. (Page 76.)

- You can do something similar by amortizing a business expense. It can be amortized over 5 to 15 years. Ex) if a chef buys recipes for $75,000, he can amortize them over 15 years and get a $5,000 deduction every year for 15 years.

- Cost segregation (depreciation): you must employ professionals to so the study, either engineers or CPAs. You don’t have to do it when you first buy the property—this allows you to do the cost segregation when your tax bracket is the highest (high tax bracket = higher tax deduction).

- You can do a cost segregation years after buying a property and then you get all of the previous years all at once. So it’s best to stack these up and use them when you are in the highest tax bracket.

- Depreciation is a tax deduction.

- Tax deductions reduce how much of your income is subject to taxes. Deductions lower your taxable income by the percentage of your highest federal income tax bracket. So if you fall into the 22% tax bracket, a $1,000 deduction saves you $220. A deduction in a high fax bracket is always better than a deduction in a low tax bracket.

- Tax credits directly reduce the amount of tax you owe, giving you a dollar-for-dollar reduction of your tax liability. A tax credit valued at $1,000, for instance, lowers your tax bill by the corresponding $1,000.

- The simplest way to determine if income is going to be taxed at a high rate or a low rate is to go back to the cashflow quadrant. In general, the left is taxed more than the right and the right is allowed tax deductions.

- Tax deductions for left side of cashflow quadrant: mortgage interest, property taxes, charitable donations, personal exemptions.

- Tax deductions for right side of cashflow quadrant: business supplies, business equipment, marketing expenses, home office expenses, vehicle use for business, meals (discussing business), travel and entertainment, mortgage interest, property taxes, charitable donations, personal exemptions

- Think about income in 5 buckets, based on tax: (1) earned income, (2) ordinary income, (3) investment income, (4) gifts or inheritance, (5) passive income.

- Earned income: Income from a job. High income taxes and high employment taxes.

- Ordinary income: Income from a pension plan, 401(k), RRSP. Taxed at the highest income tax rate.

- Investment income: Income from capital gains, interest, and dividends. And passive income from businesses and real estate. This income is taxed at a lower rate. Interest from state and municipal bonds isn’t taxable. Life insurance proceeds are also tax-free.

- Gifts or Inheritance: In most cases, the recipient of the gift does not pay taxes. The giver of the gift pays taxes when applicable.

- Passive income: Income from any business (accredited private investing) or real estate that you don’t personally manage. This income is taxed at regular tax rates, but there are many ways to reduce the amount of income that is taxed. Private equity gains are the best way to offset real estate losses.

- 1031 exchange is used to sell one property and buy another without paying taxes. If you continue to rollover properties until you die, you never have to pay taxes. You get all of the depreciation deductions without paying a tax when the property is sold. The new property doesn’t have to be exactly like the old property. You can move from single-family homes to apartment complexes to commercial property to land and back again. You can keep buying more and more expensive properties as you properties go up in value, all without ever paying tax. A like-kind exchange simply means within the same market. ex) you have to swap real estate for real estate and stocks for stocks. There are very detailed rules that you must follow when doing a 1031 exchange.

- Kids are one of the best tax shelters. When you start a business, before the business has any value, give a substantial portion of the business to your kids. This makes it free of any gift tax. Make each kid or family member an owner of the business and you may be able to get the business’ revenue taxed at only 15%. Depending on the business size, without this tax planning, it could be 2x as much. Set up trusts where you are the trustee so that you control all of the money even though you kids are the “business owners”. In the US, minor children are taxed at their parents’ rates. Instead, have your elderly parents be a part of your LLC to have their portion taxed at their lower rates. You can also give them a part of your real estate.

- For passive income, you need to do less than 500 hours per year for it to be considered passive.

- Each company can be its own taxable entity. So you should actually split up your business into a lot of different businesses and then split up the income so that each one is taxed at the lowest tax rate. Note: There MUST be a business purpose for setting up your separate corporations. You cannot set them up solely for tax savings. Ideally, you want your other service companies (companies that provide services for your business operations) to end up with net income of about $50,000, so that they are in the lowest tax bracket. Note 2: It’s important that your service companies serve 2 or more companies, so they should serve each other. Your other two companies should pay each other $10,000 for each other’s services. Note 3: there are some costs for bookkeeping for 2 extra businesses and preparing additional tax returns but it is worth it to have nearly $100,000 or more taxed at the lowest rate.

- Make a professional employment organization (PEO). This is a business that handles payroll and other Human Resources for all o your other companies. It charges other companies for this service, and their payroll costs, plus a profit. This saves you time because you only have to do payroll and Human Resource reporting in one company! Self-employed and business owners can use this +the above tip to reduce their taxes and make reporting easier.

- Make a marketing company.

- How to maintain control of your business when giving parts of it to others: Still be the manager of the LLC, majority stockholder of the S corp, or general partner of the limited partnership.

- A tax credit is the cream of the tax savings crop because it offsets your taxes dollar for dollar. It’s not like a deduction that only reduces your taxable income. It goes directly against your taxes. So if you have a tax credit of $1000, it reduces your taxes by $1000, no matter what your tax bracket is.

- Tax credits go directly against your taxes, dollar for dollar.

- Tax deductions reduce your taxable income.

- The government gives out tax credits rather than sending out checks because some people don’t know how to claim tax credits, so the government saves money.

- The government only sends out checks when it needs votes.

- There are 2 versions of tax credits. (1) A refundable credit. You can receive this credit even if you don’t have any taxes due in the first place. (2) A nonrefundable credit. You only get this credit if you actually have tax due. Most credits are like this, and for some them, if you don’t use them you can carry them over into another year.

- The government typically gives credit for these: (1) Family credits. You get a tax credit for having children. (2) Education credits. These credits go to help you offset the cost of tuition and related costs at university. (3) Working-poor credits. Usually refundable. For working poor people. Note: if you make a lot of money but know how to reduce your taxable income, you may qualify. (4) Charity credits. Sometimes you can get more money by donating and getting the write off and credit than if you hadn’t donated. (5) Investment tax credits. Credits for building low-income housing, R&D, etc. There are hundreds of different investment credits.

- Never invest in a project solely for tax benefits.

- Never start a new business solely for tax benefits. If you do, you can be audited and will not get the tax benefit. Every new business should be made to make a business process easier for you or to increase your profits.

- Government investment vehicles suck. 401(k), Roth IRA, 529 plan (educational savings for your kids), etc. They limit how much you can contribute. They control what you can do with the money in the account, even controlling how you invest the money. Some, like the 529 plan, control what you spend the money on—only certain educational expenses qualify. And there are penalties if you don’t want to follow these rules.

- There is no worse tyranny than to force a man to pay for what he does not want merely because you think it would be food for him. — Robert A. Heinlein

- You can reduce the sales tax and property tax like income tax.

- Your accountant does NOT know all of the tax benefits that are available or possible. Even the ones at top firms may not know about a specific raw materials sales tax exemption, for instance.

- Purchases not subject to sales tax in many US states: manufacturing equipment, inventory, equipment for R&D, and supplies. Always check if you can get an exception from sales tax—especially if it’s a large purchase.

- Always collect sales tax. Many people think that you don’t need to collect sales tax for online customers outside of your state. This is NOT true. When in doubt, collect sales tax. It greatly reduces your risk. If you don’t collect sales tax and the government says you have to, you pay ALL of the sales tax out of pocket.

- Reduce your property taxes: Most property taxes are calculated as a percentage of the value of your real estate. So the obvious way to reduce your property tax is to challenge the value placed on your property. This is especially true when property values are going down. Only you can protest the value they put on your property. There are time limits for protesting value (the time period is stated on your property tax bill). There are 3 main ways to claim that your property is valued less: (1) Get an appraisal. (2) Show proof that your rental income and the reduced rents of similar properties as evidence that your property should be valued lower. (3) Show that your property is being valued at a higher dollar value than a similar property. In many cases, properties of similar use, size, and location are required to be valued the same.

- Most people and tax professionals only focus on reducing income taxes, ignoring potentially bigger taxes such as sales, property, and excise taxes.

- There are as many exemptions and tax benefits in the sales and property tax rules as there are in the income tax law.

- “I have seen more businesses put out of business for uncollected sales tax than for any other tax reason.”

- Basic principles of doing business in multiple locations: You’ll be taxed where (1) you have property, (2) you have an office, (3) you have employees, (4) you may be taxed where you have contractors.

- You have to file income tax returns in any state (or county) in which you have employees.

- Operating in multiple states can work to your benefit. Doing business in states that have low or no income tax rates can help reduce your overall state taxes. When structured properly, some of your business income can become “nowhere” income and escape state tax altogether. Conversely, if you don’t know what you’re doing, you could be taxed in both your home state (or country) and the state (or country) you sell to.

- Inflation causes tax bracket creep.

- You should hear from your tax advisor a minimum of 4 times per year.

- Taxes are important but not nearly as important as personal and business goals.

Comments ()